More new records set as domestic markets bloom

17 October 2011In the four countries annual growth rates ranged between 5 and 9% in 2010, despite Mexico continuing to be tied by an umbilical cord to the weak US economy, and a once-in-a-lifetime earthquake in Chile.

For 2011, all but Chile’s economy (stimulated by post-earthquake rebuilding) will see somewhat slower growth than in 2010. But with growth rates of 4 to 8% (with Mexico on the low end of the range and Argentina on the high end), growth will continue to be at levels enviable in Europe and the US, where recessionary pressures continue to linger. Similarly other Latin American ‘tigers’, such as Peru, continue to record rapid growth in the 6 to 9% range in 2010-2011 and Colombia’s annual growth has been a respectable 4 to 5%.

Nevertheless, Latin America is not totally insulated against global economic developments beyond its borders. The debt-ceiling farce in the US in August, the single-minded Tea Party attempts to cut government spending no matter the consequences, plus the continued euro-zone crisis, all damage consumer confidence and threaten to throw global economic recovery into reverse.

Stagnation, let alone a second recession in Europe and the US, would not only ripple through China, but also through those countries that supply China’s economy with the raw materials to produce the goods to ship to global markets – such as Latin America.

The export of raw materials to China and other Asian destinations has helped fuel strong domestic growth in those supplying nations. While economic growth in countries such as China and Brazil is unlikely to slow as much as in many developed economies, the downward pressure on prices for metals, minerals and agricultural commodities will both dampen South American domestic market growth and reduce overall exports – the twin propellers of economic growth throughout Latin America.

Inflation has been a threat to Latin American economic growth since mid-2010 as oil prices jumped and Latin America’s rebound absorbed the slack (output gap) left by the 2009 recession. This has been reflected in labour shortages and higher wages in Brazil and production tightness across many industries throughout the region.

The forecast for slower economic growth over the next 12-18 months will restrain oil prices, thus relieving at least some of the energy-led inflationary pressures, while allowing investments in new productive capacity and infrastructure to come on-stream. In turn, these developments will provide the wherewithal for future low-inflation growth and thus represents a positive benefit long-term – the pause that refreshes!

Forecasts for Latin American economic growth in 2012 are all lower than for 2011. The countries listed in Table 1 show GDP climbing in a range of 3.5 to 6%. However, depending on the course charted by developed world economies this autumn (fall) and winter, following on the financial crisis experienced through the northern hemisphere summer of 2011, these forecasts could easily prove to be too optimistic; GDP growth rates just one-half of those shown are possible. Consequently, if GDP growth is indeed much lower than forecast, then industrial output growth would run well below the 3 to 6% range now projected for 2012, below the 3 to 8% expected in 2011, and down from around 10% in 2010 in all countries in Table 1 (except Chile).

In turn, these differences would have negative impacts on the outlook for wood based panel markets in Latin America.

Production in Brazil & Chile: history

However, since 2009, both Brazilian and Chilean producers of wood based panels have benefited from the resurgent economies within their region. Strong domestic markets, as well as increased exports to Asia and within the South American continent, have more than offset both the weakness in traditional export markets in Europe and North America and the negative impacts of stronger currencies.

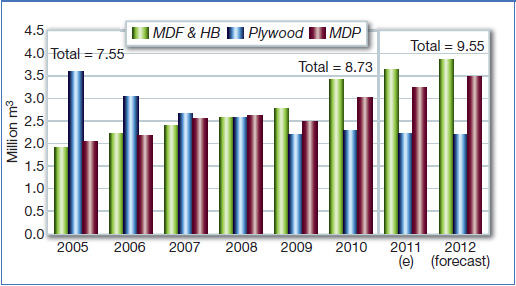

Brazil continues to lead South American production of panels, setting a new record of 8.73 million m3 in 2010, 12% above the previous record of 7.79 million m3 set in 2008.

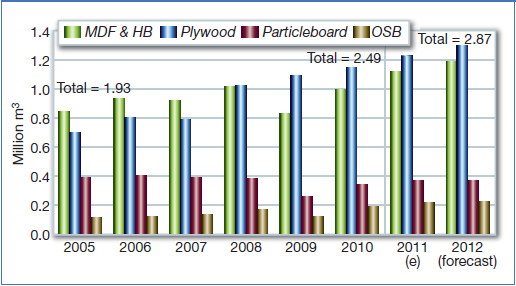

Meanwhile, total production in Chile in 2010 jumped to a record estimated 2.67 million m3, 3% higher than the previous peak of 2.59 million m3 in 2008, despite the devastation caused by the February 2010 earthquake.

While both countries recorded new production records in 2010, the dynamics underpinning the respective growth in the two countries remained significantly different.

In Chile, it was the strength in softwood plywood that drove total production higher. Since 2008, plywood production in Chile has exceeded that of any other panel type (MDF/HDF, Particleboard or OSB). In 2010, estimated plywood production of 1.15 million m3 represented 43% of total Chilean panel output. Meanwhile, MDF/HDF (including hardboard – ‘HB’ in tables) volumes of slightly less than one million m3 represented 37% of the country total; particleboard output of 0.34 million m3 accounted for 13%; and OSB output of 0.19 million m3 accounted for 7%.

In contrast, in Brazil, plywood continued to lose share of the total Brazilian market, despite a small increase in output in 2010 to 2.3 million m3 (5% above 2009, but 36% below the 2005 peak of 3.59 million m3). In turn, this plywood volume represented 26% of Brazil’s total panel production in 2010, down from 48% in 2005.

The fastest-growing panel sector in Brazil has been MDF/HDF, recording a jump of 27% between 2009 and 2010 to a record 3.04 million m3 – more than twice as large as in 2005.

Medium density particleboard production also soared in 2010, to a record 3.02 million m3; 21% above 2009 and 47% higher than in 2005.

Consequently, MDF’s share of total panel production jumped from 19 to 35% between 2005 and 2010, while MDP’s share climbed from 27 to 35%. Meanwhile, hardboard lost share, dropping from 7 to 4% as production fell from 0.51 million m3 to 0.38 million m3. Much of this can be attributed to MDF/HDF substitution.

Forecast production in Brazil & Chile

Slowing overall economic growth, plus the winding down of earthquake rebuilding in Chile, will likely dampen, if not reverse, growth in panel production in 2011-12. However, no major shake-up in the trends in panel use and production are anticipated over the next 18 months.

With no disruption of production resulting from a major earthquake, panel production in Chile will approach three million m3 in 2011 and exceed that level in 2012. Growth in plywood, MDF/HDF and OSB production are expected to be the primary drivers of this increase as producers shift a larger share of product away from domestic to export markets, particularly within South America and in Asia.

Our forecast shows plywood in 2012 representing 42% of total Chilean production of 3.1 million m3. The MDF/HDF share will be 39%; particleboard/MDP 12%; and OSB 7%.

In Brazil, total panel production is expected to exceed nine million m3 in 2011 and to approximate to 9.5 million m3 in 2012.

Weakness in plywood export markets (largely reflecting currency strength and weak European demand) will result in flat-to-lower overall plywood production. However, continued rapid growth in MDP and MDF/HDF production will more than offset this.

Production of each panel type is expected to climb to around 3.5 million m3 by 2012, with MDF/HDF continuing to exceed MDP by a small margin. Meanwhile, hardboard output will continue its slide, and increased volumes of OSB are likely to be produced in Brazil to supply growing domestic and export markets. Potentially, the growth in Brazilian

MDF/HDF production could be significantly faster than expected if domestic producers displace the still-significant volume of MDF/HDF imported by Brazil. Imports are on track in 2011 to exceed 200,000m3, after exceeding 160,000m3 in 2010. Even without additional production to replace these imports, by 2012, MDF/HDF will represent 37% of total Brazilian panel production; MDP 36%; plywood 23%; and hardboard 4%.

Despite the large growth in Brazilian consumption, pressure on domestic prices will likely remain high, largely because of the continued increase in MDF and MDP capacity throughout Brazil. Consequently, average operating rates (demand/capacity ratios) will remain too low to allow producers significant pricing power over the next few years.

However, cost-pushed increases in prices are likely (particularly if resin and energy costs escalate over the next 18 months), if only to protect relatively thin profit margins.