Plus ça change

13 May 2015There’s been a kind of déjà vue about the North American world of OSB this past year, with one major producer near to closing a merger/acquisition with another, and one of the parties involved being the same as last year.

The US housing market recovery has been solid throughout 2014, but hardly exciting. Even so, with several long-curtailed OSB mills now back on line, progress being made on a planned brand new mill for Texas, and that major merger expected to complete early this year, North American OSB producers are showing some optimism that their primary market - new home building in the US - will pick up pace.

Louisiana-Pacific (LP) Corporation's attempted acquisition of Ainsworth Lumber Co Ltd was stopped in its tracks in May 2014 when it became apparent that competition authorities' concerns were going to require either the disposal of some OSB capacity, or a lengthy and costly legal battle to push it through. LP and Ainsworth terminated their plans as cooperatively as they had worked together on them.

By the end of 2014, however, Ainsworth had a new suitor: Norbord Inc. In December, the two companies announced their plan to merge.

By all accounts - notably the investment analysts who watch the movers and shakers in the forest products market - this is altogether a different proposition.

The combination of Norbord's total OSB production capacity (including European plants) and Ainsworth's 2.54 billion ft2 will take the merged company, with some 7.7 billion ft2 of OSB capacity globally (about 7.1 billion ft2 of that in North America) ahead of LP's 5.97 billion ft2. However, there is no geographical crunch such as became apparent during the LP/Ainsworth negotiations. Competition concerns are unlikely to arise and the marriage looks set to go through, according to most of the analysts.

As we went to press, the companies said that, subject to approvals and other closing conditions, they expected the transaction to complete by the end of first quarter 2015. Until that merger is a done deal, however, little has changed in the past year in terms of OSB capacity, or the rankings of the players. LP at this time remains North America's largest OSB producer, with annual capacity of 5.97 billion ft2 (3/8in basis).

LP's Canadian OSB mills are: in British Columbia, the 820 million ft2/yr Peace Valley OSB former joint venture (JV) with Canfor which LP bought out in May 2013, and Dawson Creek (380 million ft2/yr); in Quebec, Chambord and Maniwaki, with respective annual capacities of 470 and 650 million ft2; and Swan Valley in Manitoba (410 Million ft2/yr). Chambord has been indefinitely shut since 2008.

LP's OSB mills in the US are: Sagola, Michigan (410 million ft2/yr), Jasper, Texas (475 million ft2/yr), Carthage, Texas (500 million ft2/yr), Roxboro, North Carolina (500 million ft2/yr), Hanceville, Alabama (410 million ft2/yr) and Thomasville, Alabama (750 million ft2/yr). In July 2014, it was reported that LP had sold its mothballed Athens, Georgia, OSB mill, closed since late 2009, to a wood pellet producer.

LP had also been producing about 200 million ft2 of OSB at Hayward, Wisconsin, a mill it converted to SmartSide siding production when it built the Thomasville OSB mill. However, company executives noted in a recent conference call that demand for siding is such that Hayward is going to be utilised entirely for siding production.

The company has also confirmed in recent months that it plans to convert its Swan Valley, Manitoba, OSB mill to siding by the end of 2015.

Norbord has increased its stated annual North American OSB capacity by 150 million ft2, effective from December 2014, reflecting the significant capital investment the company has made in rebuilding the wood handling end of the Joanna mill, cfo Robin Lampard said during January's Q4 conference call. That pushes up Norbord's rated capacity to 4.57 billion ft2 from 4.42 billion ft2.

Even with that increase, as things stand (prior to the Ainsworth merger closing), Norbord places itself third in the ranking of North American OSB producers. In a February 2015 presentation on its website, Norbord puts Georgia-Pacific LLC (GP) as second largest, with 19% of North America's roughly 28 billion ft2 of OSB production capacity, after LP with 22%, followed by Norbord with 16%.

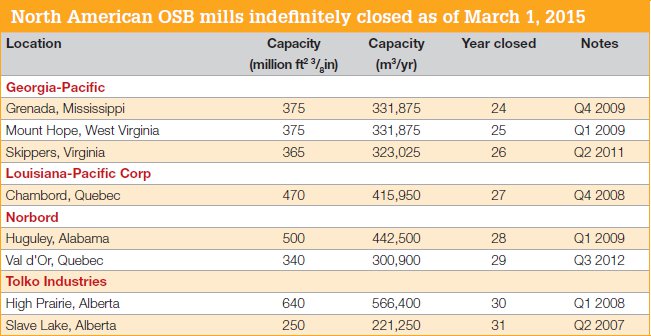

GP's rated capacity is somewhere around 5.04 billion ft2/yr, but GP is a privately held company which will not comment on mill capacities and its total OSB capacity numbers include several mills in the southeastern US that have been indefinitely closed for years. Dudley, North Carolina (170 million ft2/ yr), as noted in this report last year, appears to have permanently ceased production in October 2006, based on publicly available information.

The current capacity figure for GP assumes that other mills that at some point or other were indefinitely curtailed - Grenada, Mississippi (375 million ft2/yr), Mount Hope, West Virginia (375 million ft2/yr), and Skippers, Virginia (365 million ft2/yr) - are all still in play.

Norbord at this time last year was ramping up production at its 415 million ft2/yr OSB mill in Jefferson, Texas, since reopening it in June 2013. The company still has two OSB mills curtailed - Huguley, Alabama (500 million ft2/yr), curtailed since the first quarter of 2009, and Val D'Or, Quebec (340 million ft2/ yr), curtailed in July 2012. Executives during January's conference call said upgrade work at Huguley is continuing, but at a slower pace, given the gradual recovery in US housing, and that the mill is not expected to restart during 2015.

"Excluding our two curtailed mills in Huguley and Val-d'Or, Norbord's operating OSB mills produced at approximately 100% of stated capacity last year, compared to 95% in 2013. Three of our North American OSB mills, Bemidji, Joanna and La Sarre set annual production records," said cfo Robin Lampard during January's conference call.

Moving on from the top three, Weyerhaeuser Co still has OSB rated capacity of three billion ft2 out of six mills in the US and Canada; about 11% of the total North American production, according to Norbord's February presentation.

Ainsworth is next, with 2.54 billion ft2, as previously noted, and a 9% share of production capacity; Huber Engineered Woods LLC and Tolko Industries each have about 8% of total OSB capacity.

Huber has a rated capacity of 2.1 billion ft2 out of five OSB mills, but its 352 million ft2/ yr mill in Spring City, Tennessee, has been indefinitely closed since 2011. Although, when the mill closed, Huber described it as an indefinite closure, according to The Chattanoogan in October 2011, Spring City is not listed among the Huber Engineered Woods facilities on the parent company JM Huber Corp website, and analysts are no longer including it in their list of Huber OSB facilities.

Tolko, when all its mills are operating, has about two billion ft2 of rated OSB capacity. For much of the recession, only Meadow Lake, Saskatchewan (700 million ft2/yr) was running. However, Tolko began ramping up its state-of-the-art Athabasca Division engineered wood facility (800 million ft2/yr) at Slave Lake, Alberta, in December 2013, and brought the mill back on line in the first quarter of 2014.

The Athabasca facility, which opened briefly in 2008 before curtailing operations because of poor market conditions in 2009, has the longest continuous press in North America and is capable of producing a wide variety of products in varying lengths and thicknesses, according to the company. It is expected to reach full production capacity during Q1 this year, according to a release put out by Tolko to mark its grand re-opening on June 19, 2014.

There has still been no word from Tolko on re-opening the smaller, older, Slave Lake mill (250 million ft2/yr), which was going to be switched to value-added production to support the new Athabasca facility, nor the High Prairie, Alberta, mill (640 million ft2/yr) curtailed for market reasons in February 2008.

There has been no apparent change in status since last year of the mills owned by any of the remaining OSB companies in North America, which together account for about 7% of total OSB production, according to Norbord's chart. They are:-

- Arbec Forest Products, with total rated capacity of 700 million ft2/yr of OSB from its 294 million ft2/yr former Tembec OSB mill in St Georges de Champlain, Quebec, and the former Weyerhaeuser Miramichi, New Brunswick, OSB mill (407 million ft2/yr) acquired in 2012.

- Martco Limited Partnership (Roy O Martin), with 850 million ft2/yr from its single OSB mill in Oakdale, Louisiana.

- Langboard in Quitman, Georgia (440 million ft2/yr).

New Texas mill announced

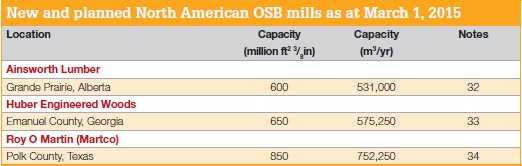

However, Roy O Martin (Martco) is to build a new OSB mill in Corrigan, in Polk County, Texas; the first major greenfield project in the North American wood based panel industry for approximately 10 years, machinery supplier Dieffenbacher announced in early April.

This has obviously stirred up interest, not least among analysts; some of them view the building of new capacity, before the US housing market recovery has gained sufficient traction or stability, as bad news for the OSB market in general.

It was known that Alexandria, Louisiana, based Roy O Martin had been looking at Corrigan for a possible new OSB mill, though its formal announcement on February 24, 2015, lacked detail on either the size of the investment or the capacity of the proposed mill. It simply confirmed that its Martco LLC unit had announced "the selection of Corrigan, Texas, as the location for a new, state-of-theart oriented strand board (OSB) facility."

Dieffenbacher is to supply a belt/Flexoplan combination forming line and (perhaps surprisingly), a 12ft x 26ft, 14-daylight hot press, rather than a continuous one. It says construction is to begin in the second half of 2015 and Martco has said that start-up is expected to be "by the fall [Autumn] of 2017". The facility will be named Corrigan OSB LLC and, according to local media coverage, the investment in it is around US$280m.

Roy O Martin's application to the Corrigan-Camden Independent School District for Appraised Value Limitation on Qualified Property describes the intended facility as being modelled on the company's existing OSB plant in Oakdale, Louisiana, which it obviously is, and having a capacity of around 800 million ft2/yr on a 24/7 operating basis.

In December, 2014, Polk County Commissioners voted to approve a 10-year tax abatement for the proposed OSB plant. During LP's recent conference call, related to its 2014 financial performance, an analyst sought input from ceo Curt Stevens on the - then only proposed - new mill. Mr Stevens appeared more sanguine about it than the analyst asking the question, who expressed amazement, "given the difficulties that the market has gone through over the last seven or eight years, including this last year, that people are talking about building more capacity."

First, Mr Stevens noted the proposal involved a private company, which can be a definite advantage when it comes to making decisions involving spending hundreds of millions of dollars in capital investment. He also noted that, if no site had been acquired yet, new OSB production from a proposed mill was realistically likely to be three or four years off, by which time, if the US housing market had rebounded beyond the 1.4 million or 1.5 million starts the OSB sector can currently support, new capacity would probably be needed.

We now know that the planned start-up is earlier than Mr Stevens suggested, thus reopening the question of timing for the market. In addition to its existing OSB mill in Oakdale, Louisiana, Roy O Martin's other panel making facilities are a plywood mill in Chopin, Louisiana, and Rocky Creek Lumber Co in Mexia, Alabama. In 2007, the company permanently closed a 350 million ft2/yr OSB mill in La Moyen, Louisiana.

Norbord/Ainsworth merger

"Some might say that the sum will be greater than the parts," was one analyst's take on the news in December 2014 that Norbord planned to merge with Ainsworth.

RBC Capital Markets noted the proposed transaction - creating a company with the largest capacity of any global OSB Producer, with around 7.7 billion ft2 - will "combine Norbord's low-cost asset base with Ainsworth's innovative value-added products, which should support new product development."

RBC also said the merger would create "the first 'truly global' OSB producer." In addition to its six OSB mills in the US Southeast and one in Quebec, Norbord has two OSB mills in Europe (Scotland and Belgium), as well as other panel production. Ainsworth's operations are located predominantly in western Canada and it ships about 82% of its output to North America (82%) and 18% to Asia, "with a leading position in Japan," RBC Capital noted.

Norbord and Ainsworth shareholders, as well as the Supreme Court of British Columbia, had all approved the proposed merger by the end of January 2015 and, according to RBC and other analysts, the deal is unlikely to hit the same kind of anti-competition hurdles that beset LP's plan to merge with Ainsworth last year.

"Although the LP/Ainsworth acquisition agreement was terminated earlier this year, we note that it was due to 'substantially lessened competition' for customers in the US PNW [Pacific Northwest] and the Upper Midwest regions," RBC Capital noted. "We suspect that the little geographic overlap limits any competition issue. We also note that the arrangement agreement allows for, if necessary, the sale of either Ainsworth's Barwick, Ontario, mill or Norbord's Bemidji, Minnesota, mill."

In a December 8, 2014, conference call on the merger announcement, Norbord executives noted that Norbord employs just under 2,000 people at 13 plant locations in Canada, the US and Europe, while Ainsworth employs about 700.

In addition to the 7.7 billion ft2 of OSB capacity, the merged company "will have an expanded breadth of operations, deeper financial resources, and increased scale," said Norbord's ceo Peter Wijnbergen. "On a pro forma basis, the combined company generated sales of US$1.63bn over the last 12 months and adjusted EBITDA of US$143m. The pro forma market capitalisation of the combined company is in the order of two billion Canadian dollars."

Norbord and Ainsworth serve separate and diverse regions with minimal overlap, Mr Wijnbergen noted. "This transaction represents an opportunity to unite Norbord's mill network, which is centred in the US southeast, with Ainsworth's assets, which are primarily in the Canadian northwest.

The combined company will be better able to serve our customers across North America and, in time, to provide customers with an expanded range of products. North America is still the leading OSB consuming market.

"Combining Norbord's low-cost assets and larger mill footprint with Ainsworth mills' innovation and value-added strength-based engineered wood products will support new product development and put us in a better position to meet the needs of our customers."

Norbord and Ainsworth management have also indicated that opportunities for the merged company to increase capacity include the restart of Norbord's currently idled mills in Huguley, Alabama, and Val-d'Or, Quebec, and the completion of the second line at Ainsworth's Grand Prairie, Alberta, facility.

"As a combined company, it will shift how we are able to think about our options that we have before us, like the room we may have to grow in Europe, the future of our currently curtailed mills in Huguley, Alabama and Val-d'Or, Quebec and the second line at Ainsworth's Grand Prairie mill. The new management team will, of course, have to spend time thinking about prioritisation and the appropriate timing and sequencing of these opportunities; but as a larger and, we think more competitive, company, we believe our growth potential is substantial," said Mr Wijnbergen.

State of the OSB market in 2014

With the exception of Ainsworth's new line at Grande Prairie, which was almost completed when the recession came along, and Martco's aforementioned new Texas mill, there are no longer any new OSB mills on the visible horizon for North America.

The rush of projects announced a decade or so ago, which were stalled by the recession, all seem to have fallen by the wayside, which is probably just as well, given the stop-and-start, some would say lacklustre, performance of the US housing market on which North American structural panels, but notably OSB, depend.

North American structural panel production in 2014 was 30.680 billion ft2, up 2.6% compared with 2013, and apparent consumption was 30.093 billion ft2, up by 2.9%, according to the quarterly Engineered Wood Statistics report released by APA-The Engineered Wood Association at the end of January, 2015.

North American OSB production was up in 2014 by 6.0%, year-on-year, to 19.885 billion ft2, with US production up 4.1% to 13.008 billion ft2 and Canadian production up 9.7%, to 6.877 billion ft2.

US apparent consumption of OSB in 2014 was 17.218 billion ft2, and Canadian consumption was 1.978 billion ft2, for a total of 19.196 billion ft2, according to APA statistics.

US exports of OSB in 2014 (excluding shipments to Canada) were up 3.8% yearon- year, to 190 million ft2, while Canadian exports to markets excluding the US were up 0.8%, to 522 million ft2. Canadian OSB shipments to the US in 2014 were up 15%, to 4.516 billion ft2.

Housing market projections for 2015

The US housing recovery gained a little traction in 2014, but at a more gradual pace than most people expected. Housing starts were up 9% year-on-year, at about 1.01 million, with single-family starts 5% higher, Norbord's cfo Robin Lampard noted in the company's recent financial conference call.

US government-supported lending agency Freddie Mac, in its February 2015 US Economic and Housing Market Outlook, released on February 18, lowered its overall projection of first quarter growth to 2.5% from 3.0% in January and lowered 2015 annual growth by 0.1 percentage points to 2.9% for the year.

Forecasts for 2015 home sales, at 5.6 million, and 2015 housing starts, at 1.18 million, were unchanged from the previous month.

House prices are expected to increase 3.9% this year on continued strong growth in house prices and relatively low inventories, which is up from Freddie Mac's forecast of 3.5% in January.

Freddie Mac's deputy chief economist, Len Kiefer, said in a release: "Despite the fact the yield curve has flattened, we remain optimistic about the course of the domestic US economy over the next year. We also do not foresee a major turnaround in the global growth picture and therefore recent trends in foreign buying of long-term US securities activity should continue. That means continued downward pressure on long-term interest rates here in the US. Even if the Federal Reserve begins raising shortterm rates later this year, don't expect to see long-term rates - including mortgage rates - increase much. This is great news for housing markets, especially headed into the spring home buying season. Lower rates help to offset some of the recent increases in house prices and keep home buyer affordability high."

Overall, builder confidence remains solid, the National Association of Home Builders (NAHB) reported on February 17, though harsh weather dragged it down slightly in February when builder confidence in the market for newly built, single-family, homes fell two points to a level of 55 on the NAHB/ Wells Fargo Housing Market Index (HMI) released on February 17.

The index gauges builder perceptions of current single-family home sales and sales expectations for the next six months as 'good', 'fair' or 'poor'. The survey on which it is based also asks builders to rate traffic of prospective buyers as 'high to very high', 'average' or 'low to very low.' Scores for each component are then used to calculate a seasonally adjusted index where any number over 50 indicates that more builders view conditions as good than poor.

"For the past eight months, confidence levels have held in the mid- to upper-50s range, which is consistent with a modest, ongoing recovery," said NAHB chief economist David Crowe. "Solid job growth, affordable home prices and historically low mortgage rates should help unleash growing pent-up demand and keep the housing market moving forward in the year ahead."

US single-family housing starts in December 2014 were at their highest level in 6.5 years, LP ceo Curt Stevens noted in the company's February conference call.

The International Builders Show in Las Vegas attracted a strong turnout of about 125,000 attendees, though Mr Stevens said there appeared to be 'universal caution' from the supplier perspective, as "We were all caught off guard by the slow pace of the housing recovery in 2014."

Suppliers are using around 1.1 million housing starts as a base assumption and, among builders, there was optimism tempered with concerns over, for example, "costs and availability of prime lots, availability of construction labour and upward pressure on labour costs, the cost of building products and margin pressure, as the ability to raise prices aggressively has dissipated," said Mr Stevens.

Just returned from the policy advisory board meeting of the Harvard Joint Center for Housing Studies, held in Washington, DC, in early February, Mr Stevens said: "I'm pleased to say that the general tenor of the meeting was the most positive in five years.

The optimism was broad-based, but the most discussed item was the expected return of the first-time home buyer, due to a variety of factors."

In the fourth quarter of 2014, Mr Stevens noted, household formations had 'shot up' to "three times what they've been averaging over the last three years. Job growth and wage increases from an improving economy get much of the credit for this.

"On the financing side, the lowering of premiums on mortgage insurance, the reemergence of the 3% down-payment loans, and more favourable credit standards are making financing more available to the firsttime home buyer."

How quickly North America's OSB producers will benefit from this strengthening of the US economy and housing market will depend on the pace at which those improvements translate into higher demand and thus higher prices for OSB.

When APA's Q4 and year-end 2014 statistics came out in January, Paul Quinn of RBC Capital forecast that OSB prices would strengthen in 2015 by 6% year-on-year and in 2016 by 13% year-on-year. However, Mr Quinn noted that, "With 3.6 billion ft2 of recent capacity additions," US housing starts of 1.2 to 1.25 million would be required to significantly tighten North American OSB markets and lead to materially higher pricing levels.

"We anticipate this occurring in 2016 at the earliest. We expect North American OSB operating rates to average 89% in FY [fullyear] 15 and 92% in FY16."