Panel Prospects

16 July 2021The global wood-based panels industry has fared better during the Covid-19 pandemic compared with average GDP and to an extent the construction industries. Frank Goecke, director of Afry Management Consulting, gave an update on the wood-based panels market to Beyond Covid delegates

Afry Management Consulting director Frank Goecke provided a wood-based panels global market update for Beyond Covid delegates and shared how the industry had coped with the Covid -19 pandemic significantly better when compared with average GDP and, to an extent, the wider construction sector.

Even without China, wood panel volumes in North America, South America and Europe dropped less significantly as a result of the pandemic compared to GDP and construction figures.

For particleboard (PB), capacity increased in 2020 while capacity utilisation dropped due to production shortages in Q2 as a result of the pandemic.

PB capacity outlook in western Europe saw some stagnation in western Europe, investments in eastern Europe, sizeable investments in North America (but also some shutdowns) and a new line in Asia Pacific.

In Q1, 2021 Afry estimates China had a PB capacity of 34.3million m3, eastern Europe 30 million m3, western Europe 27.3 million m3, 9.7 million m3 in North America, with 7.5 million m3 in South America and 10.5 million m3 in Asia-Pacific.

PB capacity utilisation in 2020 dropped by an average of 3-6%.

“We now have 80% in Europe, 70% in North America and South America, a little less than 80% in China and 70% in Asia- Pacific,” said Mr Goecke.

“We are positive about demand outlook in the next two to three years when we look at the equipment producer order books and we expect less than 5% capacity growth in PB in western Europe and more than 5% in eastern Europe, stagnation in the Americas and strong growth over the next two to three years in China – by more than 15%.”

Looking at PB production output and demand in 2020, North American production rose 1.6% and demand fell 2.7%. Europe saw a more significant decrease in both of -4.5-5%. China grew (+1.9% production and +2.2% demand), while South America saw reverses of -2.1% and -3.4% and Asia-Pacific -2.8% and -3%.

MDF market leader China has seen its MDF capacity shrink over recent years and Afry estimates its installed capacity at around 68.3 million m3 as of the first quarter, 2021.

In the past 18 months capacity shutdowns have occurred in Germany and France (removing a net 400,000m3), while eastern Europe’s capacity has increased by 400,000m3. North America has seen two investments but also two shutdowns. South America has seen an idled plant permanently shut down in the last 12 months (-400,000m3).

Mr Goecke said MDF capacity outlook in the next two to three years sees eastern Europe at +10%, North America at +5% (due to straw-based panel investments), while South America is +15% and Asia-Pacific +10%, with some stagnation in China.

MDF/HDF production overall saw a drop in 2020 despite positive development coming from the laminate flooring industry, which increased in North America and Europe. Overall, the decline in MDF was less severe than particleboard with the exception of eastern Europe.

In the OSB industry, Afry says North America has the largest capacity in Q1, 2021, with about 25 million m3, followed by eastern Europe with 8.1 million m3, while China has 3.9 million m3.

“Going forward we do expect OSB capacity to increase in almost every region, with the exception of South America and Asia Pacific,” said Mr Goecke.

Capacity outlook in the next two to three years for China is +35% and eastern Europe +15%.

In OSB production output and demand during 2020, North America production grew by +1.5% to 20.6 million m3, while demand rose +1.7% to 20.8 million m3. In western Europe, production was up +7% to 3.5 million m3 and demand rose 7.7% to 4.4 million m3. Eastern Europe recorded production growth of +5.2% and demand growth of +6.1%.

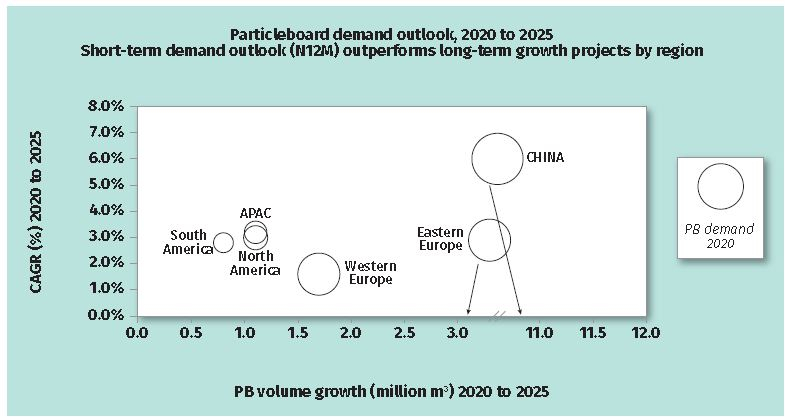

Mr Goecke forecast that the short-term pandemic recovery in construction and furniture was stronger than mid to long-term projections until 2025. Furniture production is predicted to grow across all industry segments and regions.

Western European furniture production in 2020-2025 is forecast to have +1.5% annual growth, North America +1.6% and China +5.4%, while in residential construction the growth is +1.9%, + 0.8% and over 4% respectively.

Wood-based panels producers and other players in the value chain are predicted to invest in their production lines.

Afry sees some risk of insolvencies potentially increasing in the second half of 2021 and the first half of 2022 – not necessarily in the panels sector but in other sectors, which could impact the buying behaviour of customers.