Recycled wood: waste or resource?

7 February 2019During the Wood Based Panels Symposium, held in October 2018, Silvio Mergner (Principal at Pöyry Management Consulting in Munich, Germany) asked if 'waste' wood was, in fact, a valuable raw material. He compared different countries in western and eastem Europe

Every wood product eventually ends up as waste. This is true not only for furniture, fences, sheds and wooden buildings, but also for packaging and construction materials, such as planks and concrete shuttering panels. But what does this mean for our economy?

A total of 35-40 million dry tonnes of waste wood is reaching the end of its original use every year in Europe as a whole. In times of resource constraints, renewable energy transition and circular economy aspirations, one should assume that a number of industrial processes demand the material.

However, surprisingly, this is not completely true. The majority of waste wood is being burnt or sent to landfill, with the only alternative use, on an industrial level, being the production of wood based panels, namely particleboard.

In order to make trade possible, some European states have developed classification systems for waste wood. For example, Germany is distinguishing four classes of waste wood, from untreated to heavily contaminated material.

Market transparency is generally low and varies significantly by country. On a per capita perspective, one can assume that every person, on average, accounts for 50-100kg of waste wood per year.

Collection is many-faceted: residential waste collection in municipalities; commercial waste disposal; as well as direct trade agreements between wood processing industries and recycled wood buyers.

Typically around 50% of the material is clean enough to be used in particleboard production. With better sorting, this volume could be even higher, adding extra cost to the supply chain. In total this would mean a volume of up to 20 million dry tonnes that could, in theory, be used in composite panel manufacturing in Europe; approximately half the overall raw material demand of the sector.

According to Pöyry’s estimates, only 25-30% of that is actually used in panels. But why is it not used to a higher degree? Reasons are many: Collection systems are not established and require investment. Alternative wood costs are also too competitive to justify investment in the supply chain.

However, the wood based panel industry is the only segment within today's bioeconomy where recycling of wood products has been an operational practice for years. This is particularly true in particleboard production, where supply is based almost totally on recycled wood in those European mills where fresh wood availability is a constraint.

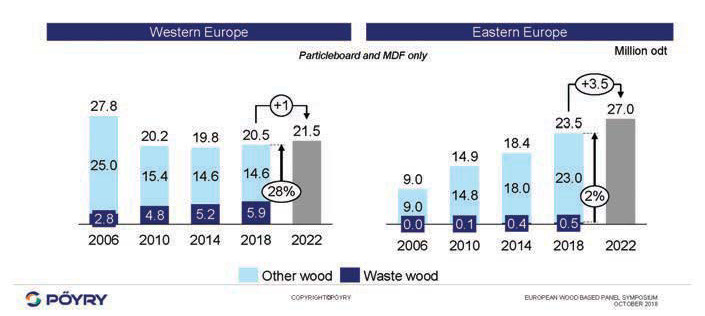

The market for composite panels in Europe has shifted from western to eastern Europe in recent years. In western Europe, consumption of particleboard and MDF is still below pre-crisis levels, while eastern European consumption has increased by 7% annually since 2006. Drivers of this shift were, among others, the cost of wood raw material. Going forward, Pöyry expects the trend will be broken and western Europe is also set to grow. And, yet again, the cost of raw material plays a role there. While the usage of waste wood for composite panel production in eastern Europe is negligible (logs are cheap), its share in the raw material mix in western Europe is a crucial element in a mill’s cost competitiveness.

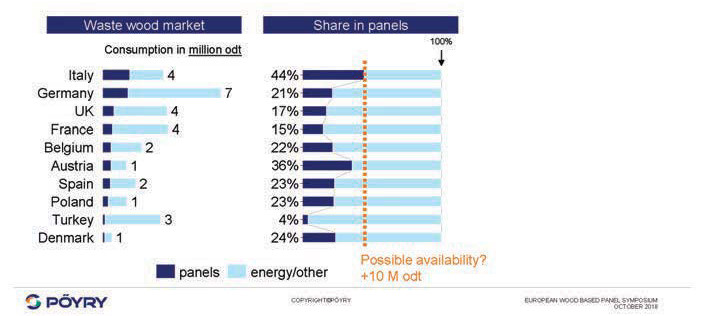

In order to understand the penetration levels in the industry better, Pöyry analysed the share of waste wood consumption in key European countries in more detail.

With an estimated 1.5-1.6 million dry tonnes per year, Italy and Germany use the highest absolute amounts of waste wood in particleboard production. The rest of the ‘top 10’ ranks lower in absolute terms, which is partly the result of lower production levels overall. Hence a comparison of the share of waste wood in the raw material mix paints a different picture.

Italy, Belgium and Denmark rank highest, certainly due to constraints (volume and price) in wood supply. If all countries shown in Figure 3 were, hypothetically, to increase the share of waste wood in the mix of particleboard manufacturing, this would result in an increased demand of more than eight million dry tonnes. Is this unrealistic? Challenges are mainly related to three dimensions:

- Quality (eg panel surface and surfacing characteristics are affected)

- Compliance / health (eg contamination levels are not harmonised across Europe)

- Value chain (mills are not always equipped to be capable of handling waste wood. Also collection, sorting and activities of suppliers and traders are not sufficiently developed).

Continuing this ‘what if’ case study, we analysed the share of waste wood used in composite panels in selected countries (see Figure 4). Again Italy stands out, with a significant proportion of above 40%, while most countries range around 15-25%. Assuming that all those top 10 countries were to achieve an allocation share like Italy’s, their combined incremental supply potential is estimated at around 10 million dry tonnes per year. While such a scenario is not unrealistic, it would require significant changes to the industry in its current state.

For businesses active in composite panels, the use of waste wood offers significant cost saving potential compared to fresh wood, and it satisfies the cascading principle like no other engineered wood product on the market. Further positive effects include, for example, the CO2 emissions balance and the easing effect on competition for wood in regions with a tight supply and demand balance.

Recycling doesn't come without challenges. Sustainability, a circular economy and our own health and safety are all noble goals. Yet, at the same time, they can create unforeseen practical problems. While the panel industry invests heavily in order to ensure that products which eventually find their way into living rooms and kitchens remain a safe alternative to other building products, quality standards are not harmonised across countries. At the same time, incentives for the use of waste wood in energy generation affect the value chain, but are handled differently in each and every country in Europe.

In this complex context, the perspectives presented in this article must not be interpreted as an outlook or clear, quantitative recommendation. Their purpose is to illustrate key regional differences; and to encourage industries and policy makers alike to utilise the vast amount of lessons learnt, and the experience which exists, in the sector.

WASTE WOOD CONSUMPTION IN THE PANELS SECTOR

The waste wood share in PB is up to 90% with significant differences

WASTE WOOD CONSUMPTION IN THE PANELS SECTOR

The waste wood share in PB is up to 90% with significant differences

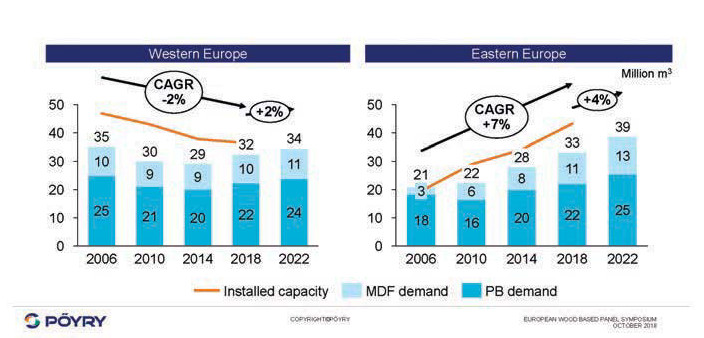

PANEL CAPACITY AND CONSUMPTION

The industry shifted capacity to Eastern Europe in the wake of the financial crisis. Western Europe starts picking up again with stable growth in Eastern Europe

PANEL CAPACITY AND CONSUMPTION

The industry shifted capacity to Eastern Europe in the wake of the financial crisis. Western Europe starts picking up again with stable growth in Eastern Europe