Capacity set to break milestone

24 October 2016This is the first edition of our two-part survey in which we list all the particleboard mills operating in Europe and North America as at the end of 2015. We also look at some ownership changes and projected capacities for the industry in the future.

If we consider first the situation in Europe, it should be noted that we have this year made a change in the countries included in our Tables 3 and 4 from last year’s report; this is more accurately to reflect economic and political realities. Whereas last year Table 3 reported capacities for the EU15 countries and Table 4 for ‘Europe outside EU15’, we now put all the EU28 countries into Table 3. The countries newly included in that grouping are the ‘recent accession’ countries of Bulgaria, Croatia, Cyprus, Czech Republic, Estonia, Hungary, Latvia, Lithuania, Malta, Poland, Romania, Slovakia and Slovenia. Some, such as Cyprus, are theoretically included, but having no particleboard mills their presence in the list is notional only.

Others, such as Poland, are major players. Britain, not yet having invoked Article 50 of the Lisbon treaty after its Brexit vote, is still a full member of the EU and of course is included in EU28.

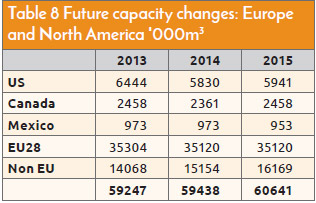

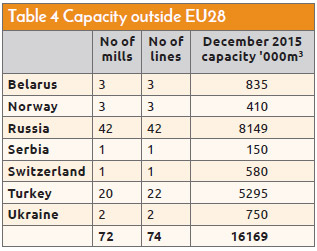

Table 4, previously recording capacity in European countries outside EU15, now records capacity outside EU 28 – so Belarus, Norway, Russia, Serbia, Switzerland and Ukraine. Tables 6, 7 and 8 are also affected.

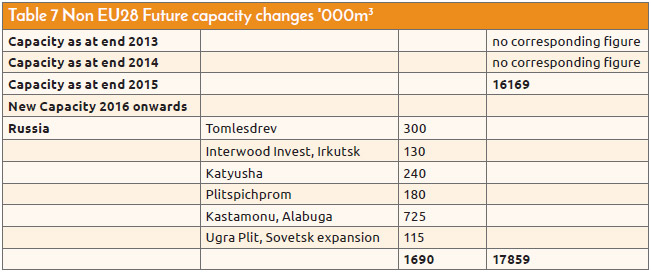

In last year’s report on future capacity changes – Table 7 – the mills at Elektrogorsk and at Bashkortostan (both operated by Kronospan, with capacities of 300,000m3 and 500,000m3 respectively) have now commenced operations and have therefore been transferred to the main listings. The Svesa group plant (600,000m3) and Ugra Plit’s Sovetsk expansion of 115,000m3 have similarly come on line and been transferred.

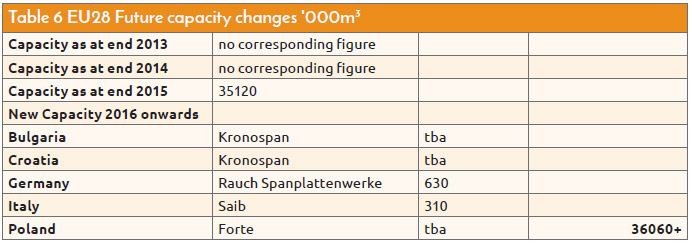

Installation of the Siempelkamp Generation 8 ContiRoll press line, of 7ft x 52m and capacity 630,000m3 per year, at the Rauch Spanplattenwerke mill at Markt Bibart in Bavaria, Germany commenced in May 2016, but the mill is still under construction, so its planned capacity of 630,000m3 per year remains in Table 6, under ‘future capacity’.

Similarly installation started in October this year of the Siempelkamp ContiRoll press line ordered by SAIB at Fossadello di Caorso in the Emilia Romagna region of Italy in 2014. The press is 8ft x 30.4m and has a designed capacity of 310,000m3 per year – a figure which also remains in Table 6 as a ‘future capacity change’ rather than one which was realised this year.

On plans for new capacity announced since our last report, one is from Polish manufacturer Fabriki Mebli Forte SA, which in March 2016 was granted approval to build a particleboard plant in the special economic zone of Sulwaki, in the north-east of the country; the required investment funding, given as €100m, is reported already to have been obtained and completion of the plant is scheduled for 2018. Its projected capacity is still to be announced. Enlarging on some of the entries in the main listings: Kronospan has announced that it intends to replace its Menznau mill by 2017 in an 80 million Swiss Franc (US$800m) investment. The capacity of the existing mill, which dates from 1981, is listed as 580,000m3; the announcement is that the ‘upgrading’ will result in a capacity of 450,000m3 – which comes out at a reduction of 130,000m3 in overall capacity. It may be that additional machinery will enable the new installation to restore or exceed the original capacity.

Note also a name-change: in March this year the company formerly known as Kronospan Switzerland AG changed its name to Swiss Krono AG. It operates as a subsidiary of Krono Holdings AG.

Also concerning name changes – or absence of change – in November 2015 the Kronospan Group bought all shares of Danish particleboard manufacturer Novopan Træindustri; but Novopan management remains as before, and still trades under the Novopan name.

In Germany, in May 2016 it was announced that Polish company Pfeiderer Grajewo has bought Nolte group’s Gemersheim-based particleboard business (capacity 450,000m3 per year), and Pfleiderer Grajewo itself changed its name – and, incidentally, its headquarters: the former to Pfleiderer group SA, the latter to Breslau. The changes are consequent from the acquisition by the Polish Pfleiderer Grajewo of its sister German company Pfleiderer GmbH.

Meanwhile French producer Darbo, whose plant at Linxe has a capacity of 450,000m3 a year, in July 2015 became a subsidiary of Gramax Capital AG.

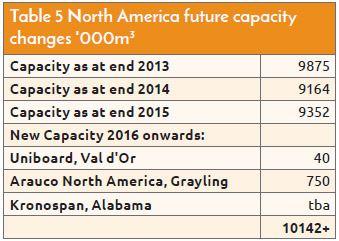

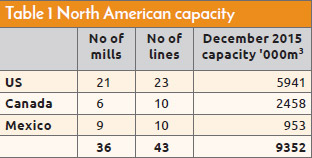

Turning now to capacity changes in North America (Table 5), we see Kronospan expanding its operations in Alabama with a mill announced in June. This will be the company’s first particleboard mill in North America – it already has MDF and laminate flooring plants there; capacity of the particleboard plant is to be confirmed. Uniboard’s Val D’or plant, and Arauco’s Grayling plant, recorded last year under the ‘future capacity’ heading, have yet to come on stream; but together with the Kronospan plant they will take the total future capacity in North America, as recorded in Table 5, to over 10,142,000m3 per year – the first time the 10-million level has been reached.

Of existing plants in North America, Arauco’s Bennetsville plant has upgraded its line to give an expanded capacity, up from the 496,000m3 per year recorded in our last year’s table of US existing plants to 584,00m3 per year, an increase of 88,000m3 per year, which is a significant upgrading (Arauco’s Albany plant records no change). The Medford plant owned by Timber Products has also expanded its capacity, from 184,000m3 per year to 207,000m3 per year. These changes together add 111,000m3 per year to North American present capacity. Timber Products has also acquired Serra Pine with its capacity of 354,000m3 per year, but since this was an existing mill the change of ownership of course does not affect capacity.

North and south of the US border some changes do need to be noted. In Canada a small mill that we removed from last year's reckoning on the grounds that it had ceased production (in January 2014) has now, happily, reopened; the revived Northern Engineered Wood Products mill at Smithers in British Columbia restores its 97,000m3 per year capacity to the total.

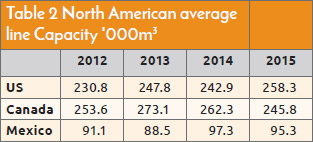

To the south, we had last year credited the Chihuahua mill operated by Masisa with a capacity of 200,000m3 per year; our latest information is that this should instead stand at 180,000m3 per year, giving an annual capacity for Mexico of 953,000m3 per year. The table for Mexico has been revised accordingly.