A year of two halves

4 April 20192018 began as the best of times and it ended as the worst of times. Industry experts now expect ample OSB supply, relative to demand, in 2019 and 2020. This report was compiled by our North America correspondents, Dick and Rich Baldwin

In the opening lines of the 1859 novel A Tale of Two Cities, Charles Dickens unwittingly described the 2018 behaviour of the North American OSB (Oriented Strand Board) industry!

“It was the best of times, it was the worst of times... it was the spring of hope, it was the winter of despair…” This analysis considers performance of the North American OSB industry in 2018, and reports on expectations of industry insiders for 2019 and 2020.

Hope blossomed for OSB producers in the first half of 2018, as builders prepared for a robust construction season, order files for structural panels grew, and wood building material prices reached record highs.

However, the hope turned to gloom by the fourth quarter of 2018 after yearly construction starts stagnated at about 1.25 million, five new OSB mills began production, and OSB prices fell by more than half from the record-high prices of the second quarter.

At the beginning of 2019, at least two mills were taking extended maintenance shut-downs. These shut-downs will lower production temporarily; and decrease inventory prior to the summer construction season. At the time of writing, no producer had announced a permanent reduction in OSB manufacturing capacity.

Looking ahead, Danushka Nanayakkara- Skillington, Assistant Vice President of Forecasting and Analysis at NAHB (National Association of Homebuilders), expects that: “Housing starts [for 2019] will be flat relative to 2018.” OSB demand and prices in 2019 are likely to parallel housing starts.

Markets ended below 2018 forecasts

Prior to the dry summer months of the 2018 building season, reputable forecasters such as NAHB, the government-owned mortgage guarantor Fannie Mae, and the largest mortgage originator Wells Fargo, forecast that 2018 housing starts would materially exceed the 1.2 million starts of 2017. Wells Fargo forecast more than 1.3 million housing starts for 2018 and almost 1.4 million for 2019.

When putting together their business plans, OSB producers also expected that new housing starts for 2018 and 2019 would be higher than actually happened. In March 2018, management of the public company Weyerhaeuser (the fourth largest OSB producer in North America) disclosed their assumption that US residential construction in 2018 would approach 1.4 million units and mediumterm fundamentals support housing starts of 1.4 to 1.5 million per year. Around that time, other publicly-traded structural panel producers shared similar forecasts with shareholders.

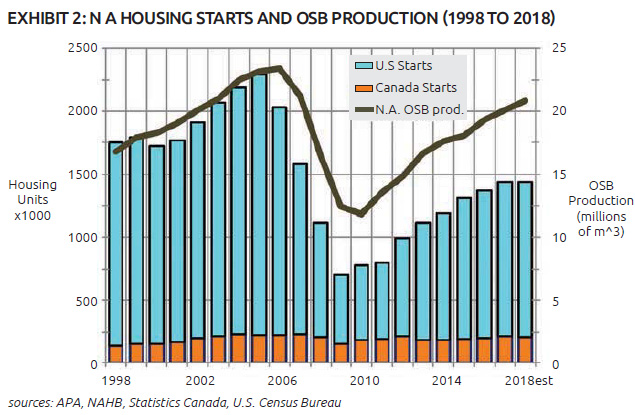

Of the 1.25 million housing units started in the US during 2018, 53% occurred in the south-east (roughly the US east of central Texas and south of Washington DC).

Compared to other regions, the south-eastern US has the most vibrant employment market and lower building costs. Therefore, housing is relatively affordable for a typical family. Three of the top five markets (Dallas/Fort Worth, Houston, and Austin) are in Texas and Texas alone has more than 15% of the nation’s building starts. The other two leading markets are the New York City and Atlanta, Georgia regions (see exhibit 2).

According to APA – The Engineered Wood Association, the primary trade group representing North American structural panel producers, North American OSB production increased 3.7% in 2018. OSB usage grew at a faster pace than housing starts. However, quarter-over-quarter growth of 5.8% in the second quarter, and 6.1% in the third quarter, decelerated to 0.7% in the fourth quarter, as the residential construction market slowed.

Rising interest rates

Nanayakkara - Skillington said: “Federal monetary budget tightening caused mortgage rates to increase faster than expected. That contributed to housing starts stalling by the end of the summer.

"Also, because of the rate increases, housing affordability declined faster than we had expected 2018 to look. These are two factors which contributed to lower housing starts for 2018 relative to initial estimates.” According to Fannie Mae, the average cost of a conventional 30-year mortgage increased from 4% in December 2017 to 4.5% in December 2018.

Wells Fargo writes that: “Higher [interest] rates, brought about by Federal [Bank] tightening last year [2018], appear to have weighed on the housing market”. In addition to higher interest rates, credit standards for mortgage loans are tighter than a decade ago.

Expansion of N American industry

Because of general expectations a few years ago for steady increases in OSB demand, several producers decided to make sizeable investments. Two greenfield, and three re-opened OSB mills started production in 2017 and 2018. Upwards of one billion dollars was reinvested in the five mills (see exhibit 3).

The rated annual production capacity of these five incremental mills exceeds 2.5 million m3.

While there is, of course, a rampup curve for a new mill to reach full production, 2018 supply increased by more than demand.

In aggregate, these mills will ultimately increase production capacity by approximately 12% (see exhibit 4).

Projections when planning these five new mills several years ago were meaningfully higher than current expectations.

Given supply growth relative to currently-expected housing start growth, OSB producers already have enough installed capacity to abundantly supply the US and Canadian markets for several years.

Three of the five new mills are in the south-eastern US and two are in Canada.

The south-east has become the epicentre of the North American forest products industry because of the abundance of wood fibre and other inputs, the perceived business friendliness of the region, and its proximity to many of the fastest-growing metropolitan regions in the US.

More than 75% of OSB made in Canada is exported – and 98% of those Canadian exports go to the US – so Canadian producers also depend on the vitality of the US housing market.

OSB mostly a commodity

OSB effectively meets the economics textbook definition of a perfectly competitive industry.

Firstly, OSB is largely a building material, which must comply with building code VPS-2 standards sponsored by the US Department of Commerce (or the Canadian equivalent CSA O325).

Secondly, individual firms have little ability to influence market prices for OSB panels.

Thirdly, OSB buyers can choose to buy from many producers at any time.

Fourthly, availability of OSB inputs such as labour, wood fibre, energy, and chemicals do not limit production.

Finally, producers freely enter and exit the market, as evidenced by many closures during the 2008 Great Recession – and several openings in recent years.

In North America, about 85% of OSB is used as a building material, in both residential and non-residential construction.

Construction applications for OSB include uses such as floors, walls and roof sheathing; and as webbing in I-joist trusses with LVL flanges. The historicallyhigh correlation of construction with the strength of the overall economy means that OSB demand is necessarily volatile.

OSB proponents are looking to expand the share of production used for industrial purposes, while researchers are studying adhesive and other process improvements which increase product flexibility.

Producers would like OSB to compete better with plywood in customer-specific end-uses, such as furniture framing and other industrial cut-to-size components.

Efforts to differentiate OSB

Given the economic characteristics of the OSB industry, producers have been challenged in achieving a lasting advantage. The desire of each producer is to develop unique attributes and markets so that their OSB competes on factors other than just price.

For example, the Huber 'ZIP' brand of OSB sheathing for roofs and walls, with a distinctive forest-green-coloured moisture barrier applied at the factory, is preferred by some builders and commands a small price premium to commodity OSB.

OSB price volatility, 2018

Market prices for many construction materials grew to record levels in the first half of 2018. Nanayakkara-Skillington states: “Building material prices have been very volatile in 2018. Builders responded by putting projects on hold. Earlier in the year, high prices for lumber and other materials added thousands of dollars in costs to a house”.

After a strong first eight months of the year, housing construction weakened in the fourth quarter and the total for 2018 more or less equalled the totals for 2016 and 17. As the pace of construction decelerated, prices for all wood products, including OSB, fell sharply, starting in the third quarter.

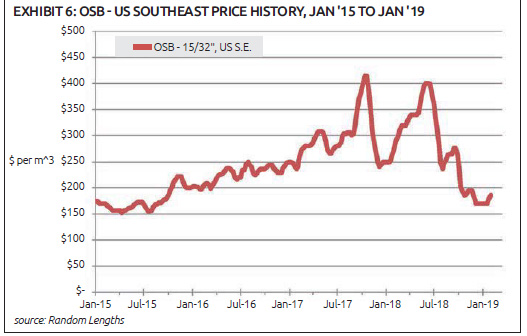

South-eastern US wholesale prices for 15/32in (approximately 12mm) OSB peaked at US$401m3 (as reported by the Random Lengths price report) in June 2018. The peak was almost 400% higher than the US$106m3 obtained during the March 2008 nadir of the Great Recession. However, OSB prices have fallen considerably since the middle of 2018; December 2018 prices were about US$170m3 (see exhibit 6).

Two major hurricanes affected the US during Autumn 2018: Hurricane Florence made landfall in North Carolina in September and Hurricane Michael came ashore in the Florida Panhandle during October.

Normally, preparing for a hurricane and then repairing the damage leads to a spike in structural panel prices. However, high inventories meant that the 2018 hurricanes did not slow the OSB price decline.

The recent volatility of wood structural panel prices reflects growing stresses in the residential construction market. Rising mortgage rates impact housing affordability. Bad weather has, at least temporarily, limited construction and demand for construction materials, and US macro-economic policy has become more uncertain (as exemplified by tensions with important international trading partners, politicians unable to agree on government spending, and uncertainty about interest rate increases).

While the US population continues to grow at a faster pace than most other industrialised countries, consumer confidence for purchasing a first home, or upgrading to a larger house, has declined.

Expectations for 2019-20

Medium-term demand for OSB in North America will continue to be correlated with housing starts. The questions become: Will housing demand grow enough in 2019-20 to absorb production increases from the five recently-opened mills, or will the incremental production cause prices to remain near current lows?

Wells Fargo forecasts that US interest rates could increase by an additional 0.5% in 2019. Higher interest rates will place downward pressure on housing starts – and demand for construction materials.

Several major forecasting services currently project more or less 1.3 million housing starts in 2019, or a few percent more than in 2018, and 1.35 million in 2020.

Otherwise, without increases in residential construction starts, or decreases in industry capacity, commodity product prices are likely to reflect the ready availability of OSB panels.

If long-term demand falls below forecasts, it is possible that higher-cost manufacturers will be compelled to permanently reduce production capacity.

In any event, a quick return to the record prices of Spring 2018 is unlikely.